Did you get any development salary or arrears of salary? In the event that truly, you may be stressed over the tax ramifications of the equivalent. Do I need to pay taxes on the total amount? Shouldn’t something be said about the tax counts of the earlier year, etc? Taxpayers who have such inquiries in their brain here is all that you have to know

At this point, you would have just made sense of that income tax is calculated on the total income of a taxpayer for a specific year. The income can either be as salary or family annuity or different wellsprings of income. In any case, there may be situations where you have gotten arrears of family benefits or pending salary during the current monetary year. It can happen that an income taxpayer gets a piece of his benefit or salary ahead of time or as arrears in any money related year, which builds his total income accordingly increment the payable taxes. In such a case, an application can be made and the surveying official can allow relief to the taxpayer. To summarize it, the Income Tax Act guarantees there is equality in the income tax chunk rates, and hence, when a bit of the income got doesn’t relate to the current year, a relief is conceded with the goal that the taxable income doesn’t increment.

To guarantee that you are not troubled with making good on extra taxes, the income tax office gives Relief U/s 89(1). In the event that you get any annuity or instalments for the earlier year, you won’t be taxed on the total amount for the current year. Basically getting you far from settling extra taxes, in light of the fact that there was a postponement in instalment.

To profit the advantages under Section 89(1) you would need to submit Form 10E. What is Form 10E would be the most evident inquiry. The subtleties of Form 10E, alongside how and for what reason to present the equivalent is given in detail underneath.

What is relief under section 89(1)?

At the point when the taxpayer gets:

1. Arrears of salary or

2. Advance salary or

3. Arrears of family annuity

At that point, such amount is taxable in the Financial Year in which it is gotten.

Be that as it may, relief under section 89(1) is given to diminish extra tax trouble because of deferral in getting such income.

How to calculate relief under section 89(1)?

Here are the means to calculate relief under section 89(1) of Income Tax Act, 1961:

1. Calculate tax payable on total income remembering arrears for the year in which it is gotten.

2. Calculate tax payable on total income barring arrears in the year in which it is gotten.

3. Calculate contrast somewhere in the range of (1) and (2).

4. Calculate tax payable on total income of the year to which arrears are connected, including arrears.

5. Calculate tax payable on total income of the year to which arrears are connected, barring arrears.

6. Calculate contrast somewhere in the range of (4) and (5).

7. The amount of relief will be the overabundance amount of (3) more than (6). No relief will be permitted if the amount of (6) is more than the amount in (3).

What is Form 10E?

For guaranteeing relief under section 89(1) for arrears of salary got, it is required to record Form 10E with the Income Tax division. In the event that Form 10E isn’t recorded and relief is guaranteed, at that point, the taxpayer is well on the way to get a notice from Income Tax office for not documenting Form10E.

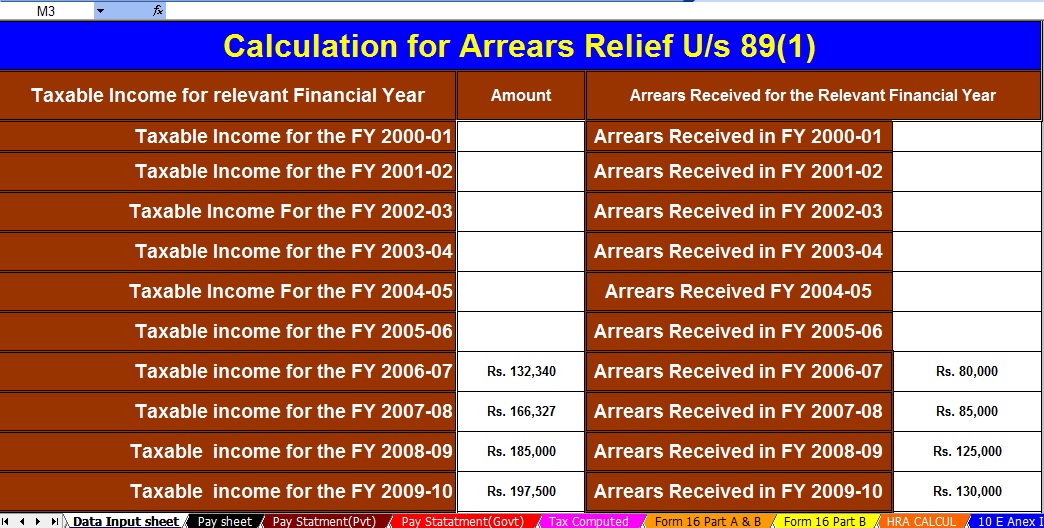

Download Automated Income Tax Arrears Relief Calculator U/s 89(1) along with Form 10Efrom the Financial Year 2000-01 to Financial Year 2020-21 (Up-to-date Version)

{kind=link}

{kind=link}