Based on eligibility, employee can avail different types of leave. If the company has a policy to carry it forward, then unavailed leave remained for a year can be carried forwarded to the next financial year. Based on employer’s policy, an employee is allowed to encash accumulated unavailed leave either during the service or after retirement / resignation. It’s known as leave encasement.

In this article we will be discussing tax on leave encasement. You will also get answers to following questions generally asked by many taxpayers:

· How is exemption on leave encasement calculated?

· What is 10 months average salary?

· How do you claim leave encasement?

Leave encasement during the tenure of service with the same employer is fully taxable in the hands of employee under the head income from salaries. However, in this case, the employee can claim relief under section 10(10AA) of income tax act, 1961.

Accumulated leave can be encased at the time of retirement. If employee has encased it at the time of retirement, then exemption is available under section 10(10AA) based on the type of employment.

Exemption on Leave encasement to government employees

For government employees entire leave encasement received at the time of retirement, whether in superannuation or otherwise, is fully exempted from tax. Government employees in this case means only state and central government employees.

This means employees of local authority and public sector undertaking will not be getting full exemption.

Due to full exemption, for government employees, leave encasement will not be included in the calculation of gross salary.

Leave encasement exemption for all other employees

In case of all other employees including employees of local authorities and public sector undertakings, least of the following will be exempted;

· Actual leave encasement received;

· Last 10 month’s average salary

· Rs 3,00,000

· Cash equivalent of unavailed leave

Cash equivalent of unavailed leave has to be calculated on the basis of maximum 30 days leave for every year of actual service rendered to the employer / completed year of service. It has to be calculated on the basis of average of last 10 months salary. Example given below will help you understand the provision better.

In case of voluntary retirement, exemption on leave encasement can also be availed under section 10(10AA)

What is average salary

Average salary = Total salary drawn by the employee during the period of 10 months immediately preceding his retirement / 10

Salary for above exemption calculation = basic salary + dearness allowance to the extent the terms of employment so provide + commission based upon fixed perception of turnover achieved by the employee

If Mr X as an employee of ABC limited retires on 31.12.2018, then average salary for the period of 10 months started from 1.3.2018 to 31.12.2018 = (total of basic salary + DA to the extent the terms of employment so provide + fixed commission as a percentage of turnover) for the period starting from 1.3.2018 to 31.12.2018 / 10

In case the employee has already claimed exemption on leave encasement for the amount received from one or more previous years then the limit of Rs 3,00,000 shall be reduced accordingly by the amount of exemption already availed. This means your exemption for the current year may be reduced based on other limits by the amount already claimed as exemption in earlier years.

As per circular number 309 dated 3.7.1981, leave salary received by the family of a government servant, who dies in harness, is not taxable in the hands of the recipient.

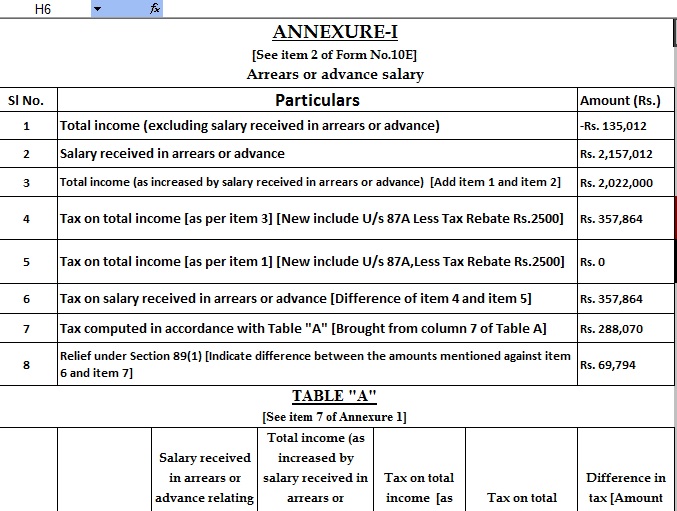

The employee can claim relief under section 89 of income tax act, 1961 in respect of leave encasement.

Example

Mr X is an employee of a private company from which he receives Rs 56,000 as leave salary at the time of retirement on 31st December 2018. Here are other details of Mr X;

· Basic Salary – Rs 5000 since 2010

· Duration of service – 20 years and 7 months

· Leave to his credit at the time of retirement – 12 months on the basis of 45 days entitlement of leave for each completed year of service.

Computation:-

| Particulars | Amount in Rupees | Amount in Rupees | |

| A | Actual leave salary | 56,000 | |

| B | Less: Exemption under section10(10AA) to the extent of least of following | ||

| 1 | 10 months salary (5,000*10) | 50,000 | |

| 2 | Maximum limit not taxable | 3,00,000 | |

| 3 | Actual leave salary received | 56,000 | |

| 4 | Cash equivalent of unavailed leave (An example given below) | 10,000 | (10,000) |

| C | Taxable leave salary (A-B) to be included in gross salary | 46,000 |

Example 1:-

· Total eligibility of leave = 20*1 month = 20 months

· Leave taken by employee = {(45 days*20)/30}-12 = 18 months

· Leave to the credit of employee = 2 months

· Cash equivalent for unavailed leave = 2 months * average of last 10 months salary = 2 * Rs 5,000 = Rs 10,000

Tax deductions for an individual

Employees are eligible for deduction under section 16 before calculating taxable salary. Following deductions from gross salary are available under section 16;

· Standard deduction of Rs 40,000/Rs 50,000.

· Deduction for entertainment allowance.

· Professional tax.

Download Automated Income Tax Arrears Relief Calculator U/s 89(1) with Form 10E from the Financial Year 2000-01 to Financial Year 2020-21 (Updated Version)

Apart from deduction under section 16, employees can also claim following deductions under chapter VI-A of the income tax act,1961 from their gross total income. But as per the Budget 2020 this exemption can entitled to those who are Opt in Old Tax Regime. New Tax Regime is not entitled this exemption as below:-

· Section 80C – in respect of life insurance, contributions to PPF, Employee Provident Fund, Tuition fees etc Max Limit Rs.1,50,000/-

· 80CCC – Pension fund

· 80CCD – Contribution to national pension system

· 80CCD(2) – Employer’s Contribution to the Employee’s Pension Fund (NPS)

· 80CCD(1B) :- Max Rs. 50 thousand , this exemption can only entitled by the Sr.Citizen above 60 Years

· 80D – in respect of medical insurance premium, Max Rs.25,000/- for below 60 Years and Rs. 50,000/- for above 60 years of age.

· 80DD – maintenance of a dependent being a person with disability including medical treatment

· 80DDB – in respect of medical treatment

· 80E – interest on loan taken for higher studies

· 80EE – interest on loan taken for residential house property

· 80G – donation to certain funds, charitable institutions etc.50% or 100%

· 80GG – Deduction in respect of rent paid Max Rs. 60,000/- P.A. who have not get any House Rent Allowance from the Employer.

· 80TTA – in respect of interest on deposits in savings accounts Maximum Amount Rs. 10,000/-